USLNG and EU Security

Ben Cahill and Jen Snyder, Center for Energy and Environmental Systems Analysis, University of Texas at Austin

White Paper, May 2026

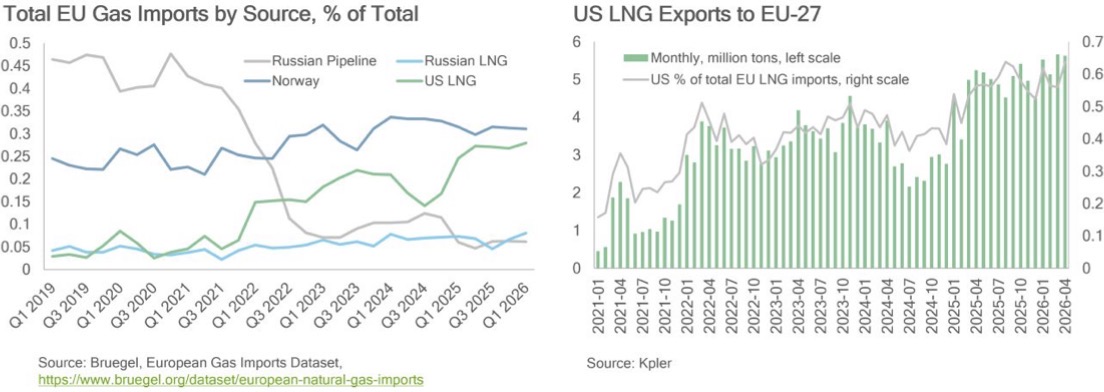

A white paper from CEESA at the University of Texas at Austin offers a timely and substantive case for USLNG’s indispensability to European energy security, and a direct rebuttal to claims that EU buyers should be wary of deepening their dependence on U.S. supply. The paper frames the analysis around two converging shocks: Qatar Energy’s force majeure declaration at Ras Laffan on March 4, 2026, which shut in 78 mtpa of liquefaction capacity, and the EU’s legislated phase-out of Russian gas by end-2027. A March 18 attack damaged two of Qatar’s 14 LNG trains (normally producing 12.8 mtpa) with repairs estimated to take at least three years. Combined with a full Gulf outage, the authors calculate ≈40 million tons in lost global supply this year alone, more than offsetting projected 2026 supply growth. EU gas storage stood at just 34% as of May 7, well below the five-year average, heading into the summer refill season.

Against that backdrop, the paper examines three risks often raised by critics of USLNG: market concentration, policy risk, and price risk. On concentration, alternatives are limited—Qatar’s planned expansion from 78 mtpa to 142 mtpa was already behind schedule before the conflict, and the war pushes realistic completion well past 2030. On policy risk, the authors largely dismiss it, citing the DOE’s 2018 policy statement and the reversal of the Biden LNG pause in Jan. 2026 as evidence of institutional and commercial constraints on any future suspension. Price risk draws the most substantive treatment: LNG feedgas may consume 20%+ of U.S. gas production within a few years, while data center construction (35+ GW underway) could add the equivalent of 35-42 mtpa in incremental gas demand. The paper’s conclusions are clear—for EU buyers, USLNG’s flexibility, hub indexation, and geographic diversity outweigh the risks, and with Qatar’s expansion timeline now in serious jeopardy, the medium-term supply picture tilts more heavily toward the United States than anyone anticipated even six months ago.

Full paper: CEESA, University of Texas at Austin →